"The grass isn't greener on the other side, it's greener on the side you water" -Kris Vallotton7/4/2018

0 Comments

Dogs of the Dow, and Index Strategies:

This article is meant as general information, and should not be considered investment advice. Past performance does not guarantee future results.

Today, the lack of hype surrounding the Dog's strategy has returned it's former edge. The strategy is no longer popular enough to impact markets, so traders can't profit from the unsuspecting pups. A similar endearment is developing toward passive index investing. Like the Dogs of the Dow strategy, indexing offers investors a chance to outperform the historical returns of many highly paid fund managers. Who can resist low fees and excellent historical returns. Indexing, like the Dogs of the Dow, is an excellent strategy. However, like the dogs, it's not without it's weakness. As the popularity of indexing strategies increases, it may predictably impact markets, not unlike the dogs, and traders won't miss the opportunity to pounce. There will always be inefficiencies in the market, but you will only find them if you look. Index investing is impacting the landscape of Wall Street. For the better. Fund managers and financial advisors are being forced to offer competitive solutions, and improved returns. Closet indexing will no longer be tolerated. The shift is already happening. Keep in mind, every rose has it's thorn. Just like the Dogs, over-popularized strategies have a pendulum effect, and eventually, they swing back. The best thing we can do with this information is to carry on with our current strategy, but be aware of the risks. Before you invest, make sure your personal debt is under control, and you have an emergency fund in place. In today's hot market, consider hedging your bets with anti-cyclical sectors; utilities, consumer staples, or healthcare. Most importantly, when there is turbulence, buckle up and stay in your seat.

What's the target?

The most important target to set in financial planning is to aim to have 25x your expected retirement living expenses, net of taxes, pensions, and social assistance, invested before you retire. The 4% rule states that generally, in retirement, you can draw 4% (inflation adjusted) from your investments, and maintain your capital throughout your lifespan. The long term real average of the stock market is ~7% returns, but during a withdrawal phase, sequence of returns risk becomes an important consideration. Why only 4%? Consider an individual with $1,000,000 retirement portfolio, planning to draw 7% per year. ($70,000) If this individual retires in a year like 2006, and draws $70,000 in a year like 2008 when certain equity markets are down by 50%, their portfolio would be reduced to less that 40% of it's original value in a single year. This level of loss would leave the retirement portfolio unsustainable at it's current withdrawal rate. In 1994, William Bengen's research showed us that even with the worst retirement timing, it is safe to draw 4% from your portfolio, and expect to maintain your capital for a 30 year retirement. Today, life expectancy keeps on improving, so considering working longer, or living on less than 4% might be necessary. Where to invest in retirement? Like any time in your life, asset allocation is highly personal. The drawdown phase of your financial lifespan is very different than the accumulation phase. During accumulation, you can afford to be exposed to far more risk. A good starting point is to hold about 2 years worth of expenses in a high interest savings account, about 8 years worth of expenses in fixed income securities, and about 15 years worth of expenses in diverse equities. This allocation of your 25 years worth of expenses divides out to a 60% equity, 40% fixed income allocation. As markets fluctuate, rebalance your portfolio to continuously maintain your desired allocation. This will result in always buying low and selling high as markets fluctuate. This is a general guideline, not a guaranteed plan for success.

Being aware of the risks we face daily, understanding the reward, and managing our exposure is something we do naturally, reasonably well. With a little bit of extra thought, we can optimize our risk exposure to improve our lives.

Putting on a seat belt in the car is an excellent risk reduction tool. In exchange for a few seconds of your time, *click* you reduce your exposure to risks associated with accidents. Maintaining your vehicle, while more costly than simply putting on a seat belt, is another way we can reduce the risk of driving. The reward is an effective way to get where you are heading in a time efficient manner. Carrying insurance on your vehicle further shields you from the financial risks associated with transportation. Some people choose a high deductible, and prefer to assume the risk of minor expenses, while protecting themselves against what could be financially catastrophic. In Canada, with most of our healthcare expenses taken care of through public health insurance, the financial risk associated with sickness is more manageable than some countries. Even so, some people prefer to carry insurance that protects against a critical illness. That way their family is able to take some time off work, or pay for treatment, without being financially burdened. Far more important than vehicle or home insurance is protecting your ability to earn an income. Being sick, or injured, unable to work would certainly be catastrophic for anyone who isn't financially independent. Just as life insurance is important for anyone who's loved ones depend on them, disability insurance is important for anyone who depends on their own ability to provide. So just as houses protect us from bears, and seat belts protect us from bananas, we need to identify risks that we are exposed to, and decide if we can afford to retain the risk, or if we need to transfer the risk via a seat belt, or insurance policy. Buckle up, and drive safe! (and also, make sure you have adequate insurance in place)

Snowball vs. Avalanche:

The debt snowball, and debt avalanche are common methods of paying off debt. The snowball approach:

The debt avalanche is the same principle as the debt snowball, only instead of listing debts from smallest to largest, list them from lowest to highest interest rate. The debt avalanche is mathematically better than the snowball, but the snowball gives you an early emotional boost. We are all more emotionally driven than we realize, so often the snowball is the better option.

In Canada, we have some amazing opportunities to invest in tax advantaged accounts. The choice can be difficult, so lets simplify it.

Here's the Principle If you deposit funds into an RRSP in a year when your marginal income tax rate is the same as your expected marginal income tax rate in retirement, the net after tax result of your investment, when comparing the same underlying fund, is the exact same as if you invested inside of a TFSA. If you deposit funds into an RRSP in a year when your marginal income tax rate is lower than your expected marginal income tax rate in retirement, the net after tax result of your investment, when comparing the same underlying fund, is not as good as if you invested inside of a TFSA. If you deposit funds into an RRSP in a year when your marginal income tax rate is greater than your expected marginal income tax rate in retirement, the net after tax result of your investment, when comparing the same underlying fund, is better than if you invested inside of a TFSA. Here's the Math Situation 1) Current marginal tax rate: 30% Expected marginal tax rate in retirement: 30% TFSA: Earn $1000 Pay $300 in tax Invest $700 at 5% growth for 30 years Net $3,127.42 RRSP: Earn $1000 Invest $1000 at 5% growth for 30 years Withdraw $4,467.74, pay 30% tax Net $3,127.42 TFSA and RRSP are equal in this situation. Situation 2) Current marginal tax rate: 20% Expected marginal tax rate in retirement: 30% TFSA: Earn $1000 Pay $200 in tax Invest $800 at 5% growth for 30 years Net $3,574.20 RRSP: Earn $1000 Invest $1000 at 5% growth for 30 years Withdraw $4,467.74, pay 30% tax Net $3,127.41 Using TFSA is optimal in this situation. Situation 3) Current marginal tax rate: 40% Expected marginal tax rate in retirement: 30% TFSA: Earn $1000 Pay $400 in tax Invest $600 at 5% growth for 30 years Net $2,860.65 RRSP: Earn $1000 Invest $1000 at 5% growth for 30 years Withdraw $4,467.74 Pay 30% tax Net $3,127.41 Using RRSP is optimal in this situation. This is a generalization, and doesn't always apply to every situation. If you are planning to take time off work, or start a business and expect to live on savings for a while, an RRSP can be used to spread your tax burden through the years of decreased income. The net result will be a lower tax bill. If your work offers a pension, this will increase your tax rate in retirement, which will decrease the benefit of using an RRSP.

Calculate Your Estimated Retirement Income Here:

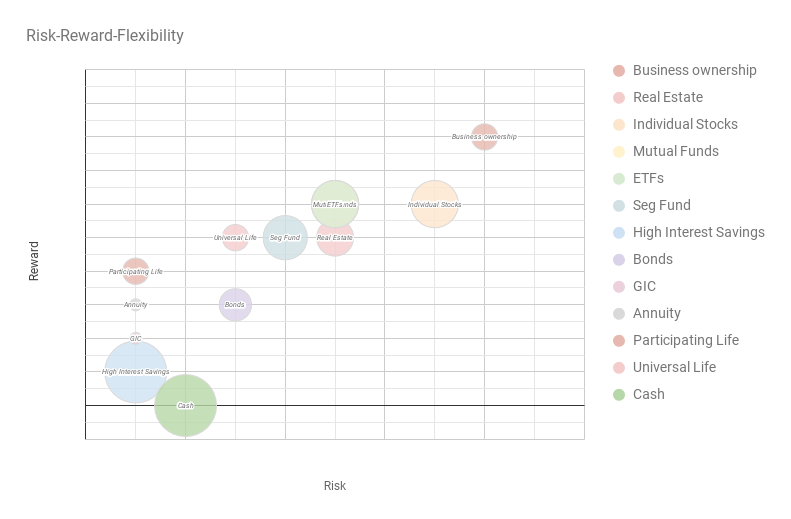

Investing can be difficult. There are so many options, it's hard to know what's best. Three key factors to keep in mind are your risk tolerance, the risk-reward profile of the investment, and the flexibility (liquidity) of the investment, or it's ability to be withdrawn when you need the funds. Generally, money that you will need within a few months should just be kept in chequing, or cash. As your time horizon increases, your optimal account changes. Money that is set aside for a goal that is up to 5 years away, like buying a house, ore your next vehicle, should be kept in a high interest savings account, or a GIC if you know the date you will need the money. Goals that are more than 5 years away, like retirement savings, should be invested in a diverse portfolio of stocks and bonds that suits your needs, goals and overall situation. If you have a strong interest in following markets, and choosing individual stocks, this should be done with money that you can afford to lose. Don't put your retirement at risk attempting to compete with professional traders. Doing so is well beyond the scope of this article. Likewise, owning your own business can offer great rewards if you are able to win at it. The range of business ownership is broad, and can't accurately be put on an investment chart, but it found a place in the top right corner, indicating high risk, high reward, and the small bubble size indicates low flexibility. This can vary from industry to industry, but is generally accurate.  **bubble size indicates investment liquidity: Large bubble = high flexibility, small bubble = low flexibility** Investment Options:

Starting in the bottom left corner of the chart, cash (your bank account), and high interest savings accounts are an acceptable choice for money that is meant for short term needs, and isn't intended for investment growth. GIC's can offer better returns than a HISA, but sacrifice flexibility to achieve the improved returns. If you can live with your money being locked in for a term, this might be the tool for you. Still in the left side of the chart, offering modest growth, with little risk are participating life insurance. Certain life insurance products offer cash value growth on your benefit, which can act as an emergency fund in retirement, or reduce estate erosion. There are a lot of factors to consider, but in some situations this is a good tool for your financial toolbox, offering modest returns, with very low risk, in exchange for flexibility. Similar to participating life insurance, universal life insurance offers tax advantages, while assuming more market exposure, allowing possibilities of more growth. Annuities are a tool that offer guaranteed payment for life. Flexibility is low, in exchange for guaranteed payments, and modest returns. Toward the middle of the chart are the type of investments found in a typical long term investment fund. Ranging from professionally to passively managed, this is the bread and butter of what most people would invest for their retirement. A well balanced, diversified portfolio of stocks and bonds that suits your needs can be an excellent investment tool. SEG funds, mutual funds, and ETF's are 3 common tools for meeting this need. Each has it's strengths and weaknesses, but can be tailored to suit your needs. Owning individual stocks, real estate, and running your own business are all outside of the scope of this simple article. Each is generally represented on the chart, just for reference. There is a huge range in all 3, and all 3 take serious commitment, education and resources. There you have it. An over simplified concept of a few common investment tools that you may or may not use in your lifetime. The most important factor that determines your financial success isn't how you invest, but rather, your savings rate. So focus on your income and your budget, and find an investment that you can life with.

In the grocery store, you can buy pre-made snacks, or you can buy raw ingredients to make your delicious snacks from, or, you can buy seed, grow rice, and process it to your desired Krispiness, and grow sugar cain, to make your own marshmallow. Some people want a pre-packaged snack that they can quick grab on their way out the door, while others may enjoy making snacks on their own.

Hyperbole aside, what is best for individuals in their personal finances can be as broad as what is best for your snacking decisions. If you have the interest and the time to educate yourself, and the gumption to create a plan, and stick with it, then self directed investing may be the path for you. Even so, seeking professional advice does bring and extra set of eyes to your situation. At the same time, there are people who don't have an interest in learning the specifics of the world of investing, and are happy to enlist a professional to send them down the best path. In any case, find a balance that you are comfortable with.

Don't spend money that you don't have. This is an incredibly difficult to grasp concept, but it is a fundamental principle on your journey toward super ultra mega hyper complex financial success. Here is a rule of thumb. When you are deciding whether or not to make a purchase, ask yourself this simple question: "Do I have the necessary funds to make this purchase?" If the answer is yes, then proceed. If the answer is no, hold off until you do have the funds. Let's be real, sometimes debt is a useful tool, but in our culture we are drowning in payments. |

Drew HonderichFinancial Advisor, Farmer, Family Guy, Musician ArchivesCategories |

RSS Feed

RSS Feed

Photo used under Creative Commons from Nederland in foto's